Between US tariffs, new Afreximbank capital, the Guyana Development Bank launch, climate insurance reform, and the CARICOM trade-liberalisation talks happening this quarter, the next four years will decide whether Guyana and the rest of CARICOM survive post-2029.

By La Caribeña News Editorial

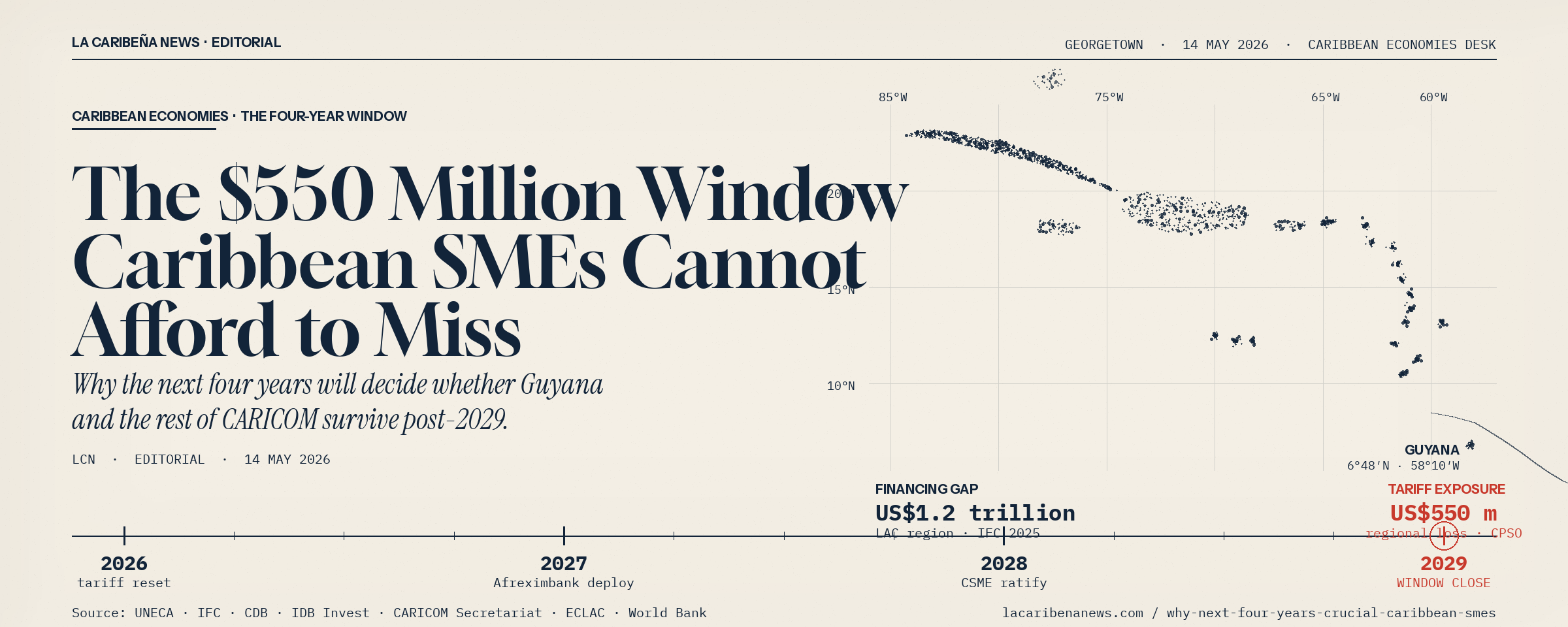

Caribbean small and medium enterprises generate roughly half of regional GDP and 45 percent of jobs across CARICOM, yet they share in a US$1.2 trillion financing gap with the wider Latin American and Caribbean region. The next four years will decide whether that gap narrows or hardens. Between now and 2029, US tariff policy, climate finance, CARICOM trade-liberalisation talks, and a wave of new SME credit lines are converging into one window. By the time it closes, the regional trade architecture will be locked in for a decade.

When an East Coast Demerara agro-processor reopened her export line last March, a single line in a US Treasury document had already taken 38 cents out of every export dollar she earned. She did not know it yet. Most Caribbean SME owners still do not.

Why 2026 to 2029 is the window

UNECA economists Wafa Aidi and Oumaima Tounchibine made the case last week that North African SMEs have four years to convert the AfCFTA opening, digital adoption, and climate adaptation into inclusive growth, or lose the chance. Their reasoning travels south. The Caribbean window has different walls, but the same clock.

US “Reciprocal Tariffs” announced in April 2025 placed a 10 percent blanket duty on CARICOM goods. Guyana caught 38 percent. Trinidad and Tobago took 15 percent, an estimated US$292 million annual export hit. The CARICOM Private Sector Organisation and the World Bank estimate the regional revenue loss at roughly US$550 million over the next few years. About 40 percent of CARICOM exports still flow to the US market.

That is not a hurricane. It is policy. And policy can be re-routed if SMEs retool fast enough.

The financing gap is not theoretical

Barbadian MSMEs make up 92 percent of formal enterprises, employ over 60 percent of the private sector, and generate 39 percent of exports. They also face a financing gap of over 77 percent, roughly three times the gap the IFC flags as restrictive for Brazil. Jamaica’s 425,000 MSMEs contribute more than 40 percent of GDP and 90 percent of private-sector activity, yet most cannot access traditional bank credit.

The capital exists. The distribution infrastructure does not. That is starting to change. Afreximbank lifted its CARICOM financing facility to US$5 billion in April 2026, with named SME on-lending facilities for Suriname, St Lucia, Grenada, and Dominica. The Caribbean Development Bank approved a US$10 million SME credit line for Trinidad and Tobago in March. IDB Invest and CDB launched a joint trade-finance guarantee programme in 2025 specifically to underwrite Caribbean private-sector exposure. La Caribeña News covered the new Afreximbank facility for Caribbean MSMEs last week and the gap between the capital available and the SMEs who actually know how to apply.

Climate risk is a balance sheet line

Hurricane Melissa caused US$8.8 billion in damages in Jamaica alone, roughly 41 percent of its 2024 GDP. The World Bank projects Caribbean climate damages to climb from 5 percent of regional GDP today to over 20 percent by 2100. The 2026 Atlantic hurricane forecast carries a 35 percent major-landfall risk for the Caribbean despite a below-normal storm count.

Insurance underwriting is shifting accordingly. Without resilience finance, climate adaptation grants, and parametric coverage built into operations before 2029, many Caribbean SMEs will not survive a single direct-impact season. IDB Invest’s US$118.9 million facility for Caribbean SME post-hurricane resilience, launched in December 2025 with the Green Climate Fund, is the kind of instrument that has to scale at least tenfold inside this window.

Guyana, Dutch disease, and the Development Bank

Guyana is the loudest test case in the region. ExxonMobil oil revenue has reshaped the country’s macro picture in under five years, with real GDP growth above 30 percent in some quarters. The risk economists keep flagging is Dutch disease: an oil-fuelled currency that prices out manufacturing, agriculture, and services, leaving the non-oil SME base weaker than it was before the boom. The counter-move on the table is the new Guyana Development Bank, framed as an SME-focused channel to keep capital flowing to non-oil sectors and protect the diversification of the wider economy.

The Guyana Manufacturing and Services Association is hosting a business luncheon on 21 May 2026 at the Guyana Marriott Hotel with Hon. Zulfikar Ally, Minister of Public Service, Government Efficiency and Implementation, to walk SMEs through the new bank’s role, eligibility criteria, and documentation requirements. If Guyana’s diversification play works, it gives every CARICOM economy a template for converting a windfall into a productive private sector. If it stalls, oil revenue funds a narrower, less productive economy and the post-2029 outlook darkens for the whole region.

Formalization and digital readiness

Procurement spending across the region is moving toward formal businesses with verifiable paperwork. In Guyana, the Local Content Secretariat made it explicit at ECONOME’s April investment forum: four documents (Business Registration, Business NIS, Owner’s TIN, Owner’s ID) separate the firms that win contracts from the firms that watch others win them. These are the formalization steps Caribbean MSMEs need to capture procurement opportunity, and the message is the same in Kingston, Bridgetown, and Port of Spain.

Digital infrastructure is following. The Bahamas Trade Commission opened a single-access digital platform for SMEs in April 2026, listing financing options, export toolkits, and trade missions in one place. These are the digital trade platforms now coming online across the region, and they reward SMEs that have their compliance documents ready before they apply.

Five moves before 2029

- Apply for a Caribbean Development Bank or Afreximbank SME line through your local commercial bank. Most owners assume they will be turned down. The new facilities were sized assuming a higher approval rate than the legacy ones. Do not filter yourself out.

- Complete formalization. If your registration, tax, and ownership documents are not in order, no facility, no procurement bid, and no export credit line will reach you. This is solvable inside ninety days.

- Diversify export exposure away from the US-only model. Intra-CARICOM, African, and EU-CARIFORUM routes now have financing behind them. The trade-reordering window favours SMEs that hold at least two viable markets by 2028.

- Price climate risk into your operations. CCRIF-linked parametric coverage and IDB resilience finance exist. Most SMEs have never been pitched these products. Ask your insurer directly.

- Track the CARICOM consultations. The Secretariat is mid-cycle on regional trade liberalisation: Georgetown ran May 7-8, Trinidad and Grenada follow May 24-28, Antigua is next. If your chamber of commerce has not surveyed you, contact them. The rule-makers are listening this quarter.

The four-year window does not give every Caribbean SME a fair start. It gives the prepared ones a runway. But the real question is bigger than which businesses survive 2029. It is whether Guyana and the rest of CARICOM survive the decade after.