An Extrapolation on Guyana's UPI Moment

Opinion | By Theon Alleyne | La Caribeña News | 26 May 2026

The author has not seen the Guyana platform. What follows is reasoned extrapolation from how India's UPI works in practice and what NPCI International has built in the twelve countries that have already adopted it.

On June 2, the rails come on. Fast Pay, Guyana's national real-time payments system, goes live across the participating commercial banks. The Unified Payments Interface integration with India's National Payments Corporation, announced the same evening by President Dr. Mohamed Irfaan Ali at the GBTI 190th anniversary gala, is the parallel piece. Whether the cross-border functionality activates on day one or weeks later has not been disclosed publicly.

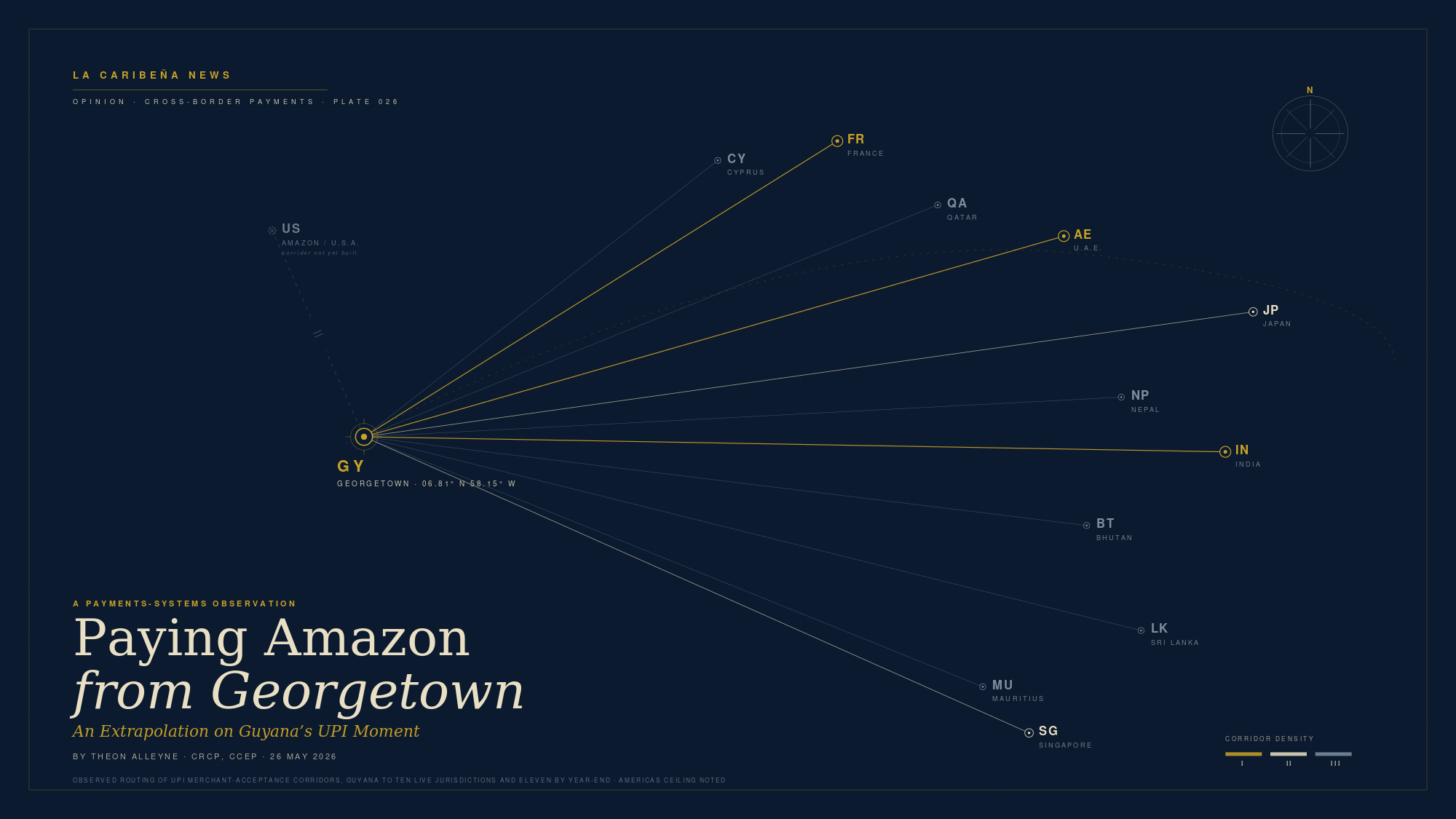

Treat the rest of this as a hypothesis, not a report. I have spent enough time inside payment systems to know what becomes possible when a country plugs into the UPI architecture. The shape of the opportunity is visible from how the same system works in Bhutan, Nepal, Singapore, Sri Lanka, Mauritius, the United Arab Emirates, France, Cyprus, Qatar, and now Japan in active rollout.

The plumbing under the "Pay" button

A UPI transaction looks instant to the user. The plumbing underneath is not.

The payer opens an app, scans a QR code or types a Virtual Payment Address, and enters an amount. The app does not call the user's bank directly. It hands the request to a sponsoring bank, which forwards it to the National Payments Corporation. The central switch resolves the recipient's address back to a real bank account and routes both legs of the transaction.

The payer is then prompted for a PIN. The PIN is captured by a secure module embedded in the app, not by the app itself. Google Pay never sees the PIN. Card and account details are tokenised, and the phone is bound to the SIM that registered the account.

The switch sends the debit instruction to the payer's bank. The bank validates the PIN, checks the balance, runs its fraud filters and debits the account. The switch then sends the credit instruction to the receiver's bank, which credits and notifies the recipient. Both apps display “successful” within seconds.

“What looks like real time to the user is real time at the user layer only.”

Interbank settlement happens later, in batches, through the central bank. The user never sees that lag because the central switch guarantees the credit. Read that twice. Most of what follows is just this model applied to a Caribbean economy.

Where Guyana plugs in

If the Guyana white-label runs the way India runs it, a Guyanese user with a Fast Pay-enabled account can do everything an Indian user does today inside the country. Send money to a family member instantly. Pay a vendor at Bourda Market without cash. Settle a contractor's invoice from a phone on a Saturday night. None of that requires Amazon. All of it adds up.

The cross-border layer is the second story, and it is more interesting than most readers realise.

The corridors that already exist

UPI is live for merchant payments in ten countries today, with Japan adding an eleventh through 2026. The list is not random. Each corridor was built because a meaningful population of Indian travellers, expatriates or diaspora wanted to pay without juggling cards. If Guyana's white-label gets wired into NPCI International's bridge architecture, those same corridors open for Guyanese users.

How fast each one opens depends on the integration work, not the rail itself. The technology is proven. The contracts are what take time.

India. The obvious first corridor. The Guyanese diaspora in the United States and the United Kingdom is large; the diaspora in India is smaller but real, and family ties run in both directions. Person-to-person remittance from Indian relatives to Guyanese accounts, and from Guyanese accounts into India, is the easiest piece of plumbing NPCI International builds. It uses the same domestic rail at both ends. Expect this to come first if it comes at all.

United Arab Emirates. Dubai is the connecting hub for half of Caribbean long-haul travel into Asia and Africa. UPI acceptance went live across UAE point-of-sale terminals through the Mashreq Bank and Network International partnership. A Guyanese traveller paying for a hotel room in Deira, a meal at Dubai Mall, or a taxi to the airport could do it from the same app they use to pay a vendor at Stabroek Market. The use case is concrete. The integration work is non-trivial.

France. This is the corridor most Guyanese have not yet thought about. UPI launched in France in 2024 through a payment acquirer called Lyra, beginning at the Eiffel Tower and extending to Galeries Lafayette ahead of the Paris Olympics. The stated expansion path is tourism and retail more broadly. France's payment infrastructure runs on the same banking system that serves French Guiana, our neighbour across the Maroni and the Oyapock. The current French UPI rollout does not yet reach Cayenne or Saint-Laurent. The architectural opening is that it could, because the rails, the regulator and the currency are the same as metropolitan France. If the Guyana white-label is plugged into UPI's France corridor and the French acquirers extend their merchant base into the overseas territories, a Guyanese person crossing the river at Saint-Laurent could pay a baker in Cayenne with the same phone they used in Georgetown that morning. That is not a 2026 outcome. It is a 2027 or 2028 conversation worth having now, because nothing about the geography or the diplomacy works against it.

Singapore. PayNow and UPI were linked in February 2023, the first live cross-border real-time link of its kind. Singapore is a frequent stop for Guyanese diplomatic and business travel and a growing one for tourism. The acquirer base in Singapore is dense. If the Guyana corridor is added to the Singapore bridge, the use case is identical to the UAE one: the Guyanese traveller pays merchants directly without a card.

Sri Lanka and Mauritius. Both went live in February 2024. These are smaller corridors for Guyanese consumers but real for two reasons. Sri Lanka is a growing budget tourism destination from the Caribbean. Mauritius is a financial centre with steady professional traffic from Caribbean regulators and compliance practitioners. I have personally watched colleagues struggle through hotel and ground transport payments in Port Louis with cards that the local merchant could not process. UPI would have closed the gap in seconds.

Cyprus and Qatar. Smaller again, but the Qatari corridor matters for sports tourism and the Cyprus one matters for the slow but persistent Caribbean professional migration into European financial services jobs.

Bhutan and Nepal. The first NPCI International deployments, in 2021 and 2022. Direct Guyanese use cases are limited, but the corridors are operationally mature and the architecture is well understood. They are the proving ground for everything that came after.

Japan, in rollout. NTT Data signed the merchant acceptance memorandum with NPCI International in October 2025. The rollout is moving in stages through 2026. By the time Guyana’s UPI integration is operational, Japan’s corridor will be in production. A Guyanese tourist in Tokyo or Osaka paying a 7-Eleven through a QR code is a more plausible 2027 scene than a Guyanese consumer paying Amazon US.

None of these corridors open automatically when Fast Pay starts on June 2. Each one needs the Guyana white-label wired into NPCI International's bridge for that country. Some bridges may be turned on quickly because they reuse India's existing acquirer relationships. Others will take longer because the acquirer on the other side has to add a Guyana counterparty to its compliance and settlement files. The point of laying them out together is that the universe of “places where I can pay with my phone” is not abstract. It is ten countries today and eleven by year-end, and Guyana's diplomacy with India has already opened the door.

What it would take to pay Amazon

Amazon does not accept UPI today at standard US checkout. The merchant acquirers Amazon uses run on Visa, Mastercard, American Express and a small set of regional networks. UPI bypasses the card networks by design. That is what makes the rail nearly free per transaction. It is also what makes US e-commerce acceptance a real integration project rather than a flip of a switch.

There is a path. NPCI International signed a memorandum with PPRO Financial in November 2021 to expand UPI acceptance into foreign markets, with China and the United States named as priority targets because together they account for roughly half of the international transactions Indian users make. Four and a half years later, that MoU has produced no US merchant acceptance at any retailer of note. It is a partnership announcement, not a checkout option.

The closer analogy for how acceptance eventually arrives is what an Indian user can already do in France or Singapore. The infrastructure on both sides knows how to handle the message. Currency conversion happens at the partner bank on each leg. The merchant accepts a local-currency payment without the card networks ever sitting in the path.

“Anyone telling you it works on day one has not read the implementation history.”

For a Guyanese user to pay Amazon US that way, three things have to be true. The Guyana white-label needs a cross-border bridge to a UPI-accepting jurisdiction. That bridge needs PSP-level integration with a US merchant acquirer that Amazon uses. And Amazon has to accept UPI as a checkout method, which it has not announced anywhere. None of those three are impossible. None of them happen on June 2 either.

The honest order of operations

If you put the corridors in order of how likely they are to open for Guyanese users, the picture comes into focus. Domestic Fast Pay activates on June 2 and changes how money moves inside Guyana within weeks. India-Guyana person-to-person remittance is the natural second wave, plausible within the first year because the diplomatic groundwork is already done. The travel corridors are next, with the UAE, France, Singapore and Japan as the most consequential for Caribbean travel patterns. French Guiana is the wild card because the geography is right there and the acquirer relationships in metropolitan France are the same ones that would extend across the river. US e-commerce is the corridor most readers will be asking about, and it is the corridor that is furthest out.

The bigger reading

Italy's digital payments experience showed that even a one-percentage-point lift in adoption can move GDP measurably. India has delivered that result at scale, with the International Monetary Fund crediting UPI with 49 percent of global real-time transactions. Brazil’s Pix has produced a comparable lift, with 91 percent of adults active on the rail four years in. The point of importing this architecture is not, in the first instance, to enable Amazon shopping. It is to make every domestic transaction faster, cheaper and more visible, which is the precondition for everything else. Once that base is solid, the cross-border corridors layer on top of it one by one as the contracts are signed.

Trinidad signed the same kind of memorandum with NPCI International in September 2024 and has not gone live. WapiPay's Jamaica entry is a remittance play, not a domestic rail. Guyana is doing both at once and is now plugged, at least diplomatically, into a corridor map that reaches three continents.

The day-one read is straightforward. Fast Pay solves the local problem. The UPI integration opens the door to ten existing cross-border corridors and an eleventh that activates this year. Whether the door opens onto Mumbai first, Dubai second, Cayenne third or New York last is an integration question rather than a technology question.

The technology has already been proven at a scale ninety times the size of this economy. The next move is the integration work nobody can announce until the contracts are signed. On June 2 we will see whether the rails carry the traffic. The Amazon answer comes later. The corridors that already exist will arrive first, and they may be the bigger story. Happy "Financial" Independence Guyana!

BY THEON ALLEYNE

Founder, EICCIO Advisors | Author, Letters to a Compliance Officer

Theon Alleyne, CRCP, CCEP, is the Founder of EICCIO Advisors, a compliance advisory firm based in Georgetown, Guyana, providing compliance strategy and financial crime risk advisory services to financial institutions across the Caribbean. A former securities regulator with experience at NYSE American, NASDAQ and FINRA, he specialises in anti-financial crime compliance, fraud prevention and sales practice conduct risk. Alleyne is a member of the International Association of Financial Crimes Investigators (IAFCI). His book, Letters to a Compliance Officer: What They Never Told You About the Job That Protects Everyone, published by Team Shaw Caribbean Press, is available on Amazon, Apple Books, Barnes and Noble, Kobo and ten additional platforms worldwide.