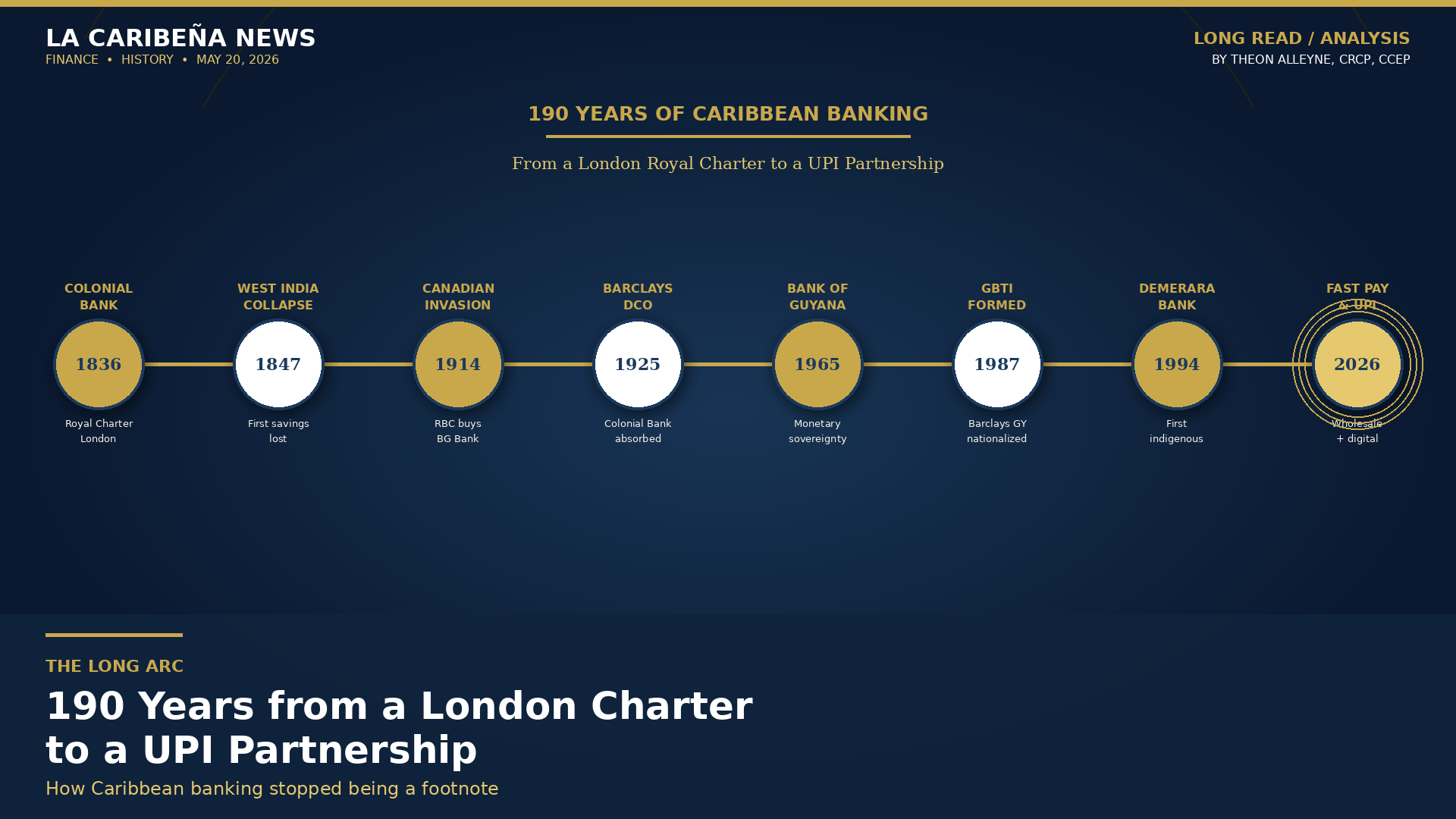

In 1836, the Colonial Bank was chartered to finance the British West Indies. In 2026, Guyana licensed three wholesale banks and prepared to launch Fast Pay with UPI. The 190-year arc closed Saturday night at GBTI’s Anniversary Gala.

Two banks were chartered in 1836. One of them you have heard of. The other you almost certainly have not.

The first, the Colonial Bank, was incorporated by Royal Charter in London on 1 June 1836, with its head office at 16 Bishopsgate and a subscribed capital of two million pounds. Within twelve months, it had opened thirteen branches and agencies across Trinidad, Jamaica, Barbados, British Guiana, and St. Thomas. The second, the British Guiana Bank, was chartered locally in the same year. It served Demerara, Berbice, and Essequibo as a domestic institution until 1914, when the Royal Bank of Canada acquired it.

President Dr. Mohamed Irfaan Ali spent a meaningful portion of his Saturday night remarks at GBTI’s 190th Anniversary Gala tracing the longer history of Caribbean banking. He started in 1836. He took the audience through emancipation, the absorption of the Colonial Bank into Barclays, the post-independence wave of state ownership, the 1990s privatizations, and into the present moment with Fast Pay and the UPI partnership launching on June 2 and the licensing of Citibank, Crown Agents, and One Americas. The arc is 190 years long.

Most of that arc has been told as a footnote in someone else’s story. London’s. Toronto’s. New York’s. Saturday night was the first time in a long time that a sitting CARICOM head of state laid out the full sweep and put Caribbean banking back at the centre of its own narrative. This piece is an attempt to do the same on paper.

Before formal banking: a system that ran without coin

Before the 1830s, the British Caribbean economy was financed almost entirely from London. Plantation owners transacted with European buyers through bills of exchange, book entries at merchant houses, shipping arrangements, and pensions and mortgages settled in London. Sugar, rum, and cotton moved one way. Supplies moved the other. London merchant-bankers took the spread and the risk.

There was no formal banking inside the colonies. There barely needed to be. A planter who wanted to pay another planter did not move coin; he wrote a draft against his London agent, the agent debited his account, and the credit appeared on the recipient’s London ledger. The physical economy ran on hands and machinery and ships. The financial economy ran on paper in another hemisphere.

The President made the same point on Saturday night: “Imagine all of these transactions without a single coin changing hands physically.” It is a strange thing to picture, but it was the reality of how the British West Indies financed itself for the better part of two centuries.

Emancipation as the forcing function

The abolition of slavery in the British Empire in 1834 changed this. Wages had to be paid in cash. Newly free workers needed access to currency, however modest. Plantation accounting moved from book entries between London and the estate to actual payroll inside the colony. Governments needed cash to fund expanding public administration. The old planter-credit system, designed for a closed circle of European merchants and slave-owners, could not absorb the new reality.

Formal banking became necessary, urgently. The Colonial Bank was created to meet that need.

It was a strictly commercial bank by charter, which meant it could finance trade, accept deposits, and provide short-term advances, but was largely prohibited from lending against real estate or providing long-term development capital. It financed crops, exports, imports, shipping, and commerce. It connected Caribbean trade to the wider imperial financial network. By the 1850s, it was the dominant financial force throughout the British West Indies.

What it could not do was finance the Caribbean’s own development.

The forgotten collapse of 1847

There was an early Caribbean bank that tried to do more. The West India Bank, founded in Barbados in 1840, offered interest on deposits and attracted the savings of recently emancipated Caribbean people. It was the first generation of formal banking explicitly aimed at ordinary depositors in the region.

It failed in December 1847. The 1846 Sugar Duties Act, passed in London, removed preferential tariffs on West Indian sugar and crashed prices. The West India Bank could not absorb the losses. It collapsed within a year. The first generation of free Caribbean depositors lost their savings to the first generation of post-emancipation banks.

This story is not in most Caribbean history textbooks. It belongs in this one. Trust in banking is built over generations and broken in a quarter. The West India Bank collapse left a memory of risk in Caribbean households that took most of a century to repair, and arguably never fully has.

The Canadian invasion, 1889 to 1914

The next chapter is not British. It is Canadian.

In 1889, the Bank of Nova Scotia opened a branch in Kingston, Jamaica. It was the first Canadian bank in the Caribbean, and it set off a wave. The Royal Bank of Canada followed in Cuba in 1899, then across the region. By 1914, RBC had purchased the British Guiana Bank outright, ending 78 years of independent local banking in Demerara, Berbice, and Essequibo. By the 1950s, RBC had 39 Caribbean branches and the Bank of Nova Scotia had 25.

The Canadians out-competed the British on something simple: relationships. They moved faster, took on consumer business that the Colonial Bank had largely ignored, and built networks that survived independence by decades. For most of the twentieth century, Caribbean banking was Canadian banking. Almost nobody outside the region remembers this.

Colonial Bank into Barclays, 1916 to 1925

The Colonial Bank itself entered its final phase between the world wars. The Colonial Bank Acts of 1916 and 1917 widened its charter first across the Empire and then globally. In December 1917, it signed a working arrangement with Barclays Bank, which had been quietly accumulating control. By 1925, Frederick Goodenough, Barclays’ chairman, secured an Act of Parliament that re-incorporated the bank as Barclays Bank (Dominion, Colonial and Overseas), known thereafter as Barclays DCO. The Colonial Bank brand was extinguished. Barclays DCO operated under that name until 1971.

For the next sixty years, the Caribbean’s largest bank by branch network was either Canadian or British, with Citibank and Chase establishing smaller specialist presences from the United States. Caribbean banking had become a footnote in someone else’s annual report.

Sovereignty arrives: the Bank of Guyana, 1965

The Bank of Guyana Ordinance No. 23 of 1965 brought monetary sovereignty to a country that was still seven months away from formal independence. Operations commenced on 16 October 1965. The first Governor, Dr. Horst Bockelman, was seconded from the Deutsche Bundesbank. The first Bank of Guyana currency notes were issued on 15 November 1965, replacing the British Caribbean Currency Board notes that had served the colony for decades.

This was the first time in 129 years that the country could set its own monetary policy. The Bank of Guyana was, and remains, the institution underneath every subsequent change in this story. Every bank licensed since 1965 has been licensed by it. Every payment rail that goes live in this country, including Fast Pay on June 2, is approved by it.

Guyana achieved political independence from Britain on 26 May 1966. The bank had already been doing the work for seven months.

The state-ownership wave, 1970 to 1987

The 1970s and 1980s in Guyana brought the most aggressive nationalization sequence in the English-speaking Caribbean. The Guyana National Cooperative Bank (GNCB) was founded in February 1970 as a state development bank. The Guyana Agricultural and Industrial Development Bank (GAIBANK) followed in the early 1970s.

Then came the foreign-bank takeovers. In 1984, the Royal Bank of Canada’s Guyana operations were nationalized and rebranded as the National Bank of Industry and Commerce (NBIC). In 1985, Chase Manhattan’s branches became Republic Bank (no relation to the later Trinidad-headquartered institution of the same name). In 1987, Barclays’ Guyana branches were nationalized to create the Guyana Bank for Trade and Industry, or GBTI, which opened to the public on 1 December 1987.

GBTI’s birthday, in other words, is not 1836. The institution that hosted Saturday night’s 190th Anniversary Gala is genealogically descended from the Colonial Bank’s 1836 charter, but the entity called GBTI is 39 years old, not 190. The 190 figure measures the bloodline. It does not measure the legal entity. Both numbers are correct in their own way, and the President was right to honour the longer one.

Privatization and the indigenous era, 1991 to 1998

The IMF Economic Recovery Programme that began in 1989 forced a complete restructuring of the Guyana banking sector. GBTI was privatized in 1991. By 1994, it was fully in private hands.

What happened next was historic. On 20 January 1992, Demerara Bank Limited was incorporated. On 12 November 1994, it was officially inaugurated by President Cheddi Jagan. It was Guyana’s first indigenous commercial bank, founded by Dr. Yesu Persaud of Demerara Distillers. For the first time since 1836, a country that had been served by London and then Toronto and then London again had its own bank.

In 1993, Citizens Bank Guyana was incorporated as a wholly-owned subsidiary of Citizens Bank Jamaica. It opened in 1994. In 1998, Banks DIH acquired a controlling 51 percent stake, completing the indigenization.

By the late 1990s, Trinidad’s Republic Bank Limited had also positioned itself for return entry. In late 1997, it acquired 51 percent of NBIC. In October 2003, that stake rose to 65.1 percent. On 2 June 2006, the institution rebranded as Republic Bank (Guyana) Limited, the form it carries today.

In a decade, Guyana had gone from a financial sector dominated by foreign-owned subsidiaries and a handful of state banks to one with two indigenous commercial banks, a re-privatized GBTI, and a foreign acquisition by another Caribbean institution. The economic geography of Caribbean banking shifted south for the first time in 129 years.

The present moment

That is the arc that runs into Saturday night at GBTI.

Within twelve months of each other, the Bank of Guyana has licensed Citibank N.A., Crown Agents, and One Americas as wholesale institutions, and approved Fast Pay and the UPI partnership with India for launch on 2 June 2026. Wholesale banking, real-time retail payments, and global interoperability are arriving together. This has not happened in a single eighteen-month window anywhere else in the Caribbean.

The President called it a “new golden era of banking.” Read against the 190 years that preceded it, the phrase is the right scale.

How the eras compare

What 190 years tells us about what comes next

Three things are worth pulling from the long arc.

The first is that Caribbean banking has changed hands roughly every two generations. London 1836 to 1925. London and Toronto 1925 to 1970. State 1970 to 1991. Privatized and indigenous 1991 to today. Wholesale and digital, starting now. The interval is shortening. The current transition is happening in less than five years rather than fifty.

The second is that ordinary people lose savings when the system fails. The 1847 West India Bank collapse is the case study. The 1980s nationalization wave is the case study. The de-risking decade between 2015 and 2024, when Caribbean correspondent banking relationships were severed by global compliance pressure, is the most recent case study. Whatever rails Guyana builds next, the design question that matters most is whether the system survives the inevitable shock.

The third is that we have not had a serious in-country wholesale banking layer since the Colonial Bank’s branch network operated through Barclays DCO. For most of the modern era, the country has been a footnote in someone else’s balance sheet. Citibank, Crown Agents, and One Americas, properly executed, end that. The infrastructure of Fast Pay and UPI, properly executed, ensures the gains reach a market vendor in Bourda and a fisherman in Anna Regina, not only the corporate clients in Camp Street.

The President framed Saturday night as a moment of confidence. The historical record suggests confidence is the right word. The 190-year arc was not a straight line. It bent away from the Caribbean for most of it. It has, finally, bent back.

FAQ

Who chartered the Colonial Bank? The British Crown, by Royal Charter, on 1 June 1836 in London. The bank operated across the British West Indies and was eventually absorbed by Barclays Bank, becoming Barclays DCO in 1925.

Was there a domestic bank in British Guiana before 1914? Yes. The British Guiana Bank was chartered in 1836, the same year as the Colonial Bank, and operated independently until the Royal Bank of Canada acquired it in 1914.

When was the Bank of Guyana founded? The Bank of Guyana commenced operations on 16 October 1965, seven months before Guyana’s political independence on 26 May 1966. The first Governor was Dr. Horst Bockelman, seconded from the Deutsche Bundesbank.

When was Demerara Bank founded? Demerara Bank Limited was incorporated on 20 January 1992 and officially inaugurated on 12 November 1994 by President Cheddi Jagan. Its founder was Dr. Yesu Persaud. It was Guyana’s first indigenous commercial bank.

When did GBTI start? GBTI opened to the public on 1 December 1987, formed from the nationalization of Barclays’ Guyana operations. Its genealogical bloodline runs back to the Colonial Bank’s 1836 charter, but the legal entity is 39 years old.

What happened to the West India Bank? Founded in Barbados in 1840, the West India Bank collapsed in December 1847 following the Sugar Duties Act of 1846, which crashed Caribbean sugar prices. It was the first formal Caribbean bank to attract ordinary deposits from recently emancipated savers. They lost their savings.

By Theon Alleyne

About the Author

Theon Alleyne, CRCP, CCEP, is the Founder of EICCIO Advisors, a compliance advisory firm based in Georgetown, Guyana, providing compliance strategy and financial crime risk advisory services to financial institutions across the Caribbean. A former securities regulator with experience at NYSE American, NASDAQ and FINRA, he specialises in anti-financial crime compliance, fraud prevention and sales practice conduct risk. Alleyne is a member of the International Association of Financial Crimes Investigators (IAFCI). His book, Letters to a Compliance Officer: What They Never Told You About the Job That Protects Everyone, published by Team Shaw Caribbean Press, is available on Amazon, Apple Books, Barnes and Noble, Kobo and 10 additional platforms worldwide.